Why Should You Buy a Pension Plan from Policybazaar

Pension Plans Vs. PPF Vs. NPS Vs. Saral Pension Yojana

Frequently Asked Questions

Page Progress

Retirement - Pension Plans in India 2025

Pension plans are especially designed to secure a steady income for your post-retirement years. It helps maintain a stable lifestyle by covering various expenses like medical, groceries, property taxes, emergencies, etc., ensuring financial security. The right pension and retirement plan can help you live a stress-free financial life after you retire.

Read more

Peaceful Post-Retirement Life

Tax-Free* Regular Income

Wealth Generation to beat Inflation

4.8++ Rated

10.5 CroreRegistered Consumer

51 PartnersInsurance Partners

5.3 CrorePolicies Sold

We are rated++

10.5 Crore

Registered Consumer

51

Insurance Partners

5.3 Crore

Policies Sold

Start Investing ₹10k/Month & Build a corpus of ₹1 Crore# on Retirement

Retirement Plans are designed to build a reliable income stream even when you stop earning. In general, there are 2 types of plans:

Pension Plans

Pension plans are investment plans in which your money grows through regular or lumpsum payments, ensuring financial stability and peace of mind during your retirement years. Starting early with a well-chosen pension plan allows you to build a substantial retirement fund.

Annuity Plans

Annuity Plans offer regular monthly payouts to individuals for the rest of their lives. In these plans, you put regular money during the accumulation phase. At the end of the plan tenure, you buy an annuity so that you receive your accumulated corpus at regular monthly intervals as per your selected plan. This helps you receive guaranteed income whenever you stop working.

It is important to research and select the most suitable pension plan to meet your individual needs.

The following list will help you to choose the best pension plan among various options available:

Pension Plans in India

Entry Age

Maturity Age

Policy Term (PT)

Minimum amount to Invest (yearly)

Bajaj Allianz Life LongLife Goal

18 - 65 years

99 years

99 years minus Entry age

Rs. 25,000 p.a.

Get Details

Canara Promise4Growth - Life

18 - 60 years

18 - 80 years

10-30 years

Rs. 12,000 p.a.

Get Details

Edelweiss Life Tokio Wealth Secure Plus

18 - 60 years

18 - 70 years

5-25 years

Rs. 24,000 p.a.

Get Details

HDFC Life Click 2 Wealth

18 - 60 years

18 - 99 years of age

20 - 64 years

Rs. 12,000 p.a.

Get Details

HDFC Life Smart Pension Plan

25 - 70 years

40 - 80 years

10 - 55 years

Rs. 30,000 p.a.

Get Details

ICICI Prudential Life Signature

18 - 60 years

18 - 75 years

10-30 years

Rs. 30,000 p.a.

Get Details

ICICI Prudential Signature Pension

25 - 65 years

40 - 80 years

20 - 55 years

Rs. 60,000 p.a.

Get Details

Kotak E-invent - Retire Rich Plan

18 - 50 years

28 - 60 years

10/ 12/ 15/ 20 years

Rs. 24,000 p.a.

Get Details

Max Flexi Wealth Advantage Plan

18 - 50 years

18 - 75 years

10 - 40 years

Rs. 24,000 p.a.

Get Details

Max Life Online Savings Plan

18 - 60 years

85 years

5 - 52 years

Rs. 12,000 p.a.

Get Details

Max Life SWP - Long Term Income Plan

18 - 60 years

60 - 85 years

60 - 80 years minus Entry Age

Rs. 11,000 p.a.

Get Details

PNB Goal Ensuring Multiplier

18 - 60 years

99 years

39 - 99 years

Rs. 18,000 p.a.

Get Details

Tata AIA Fortune Guarantee Pension

18 - 75 years

40 - 85 years

5 - 15 years

Rs. 12,000 p.a.

Get Details

Tata AIA Fortune Maxima

18 - 60 years

100 years

100 minus issue age

Single: Rs. 25,000; Limited: Rs. 12,000 p.a.

Get Details

See More Plans

Disclaimer: ≈ Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. This list of plans listed here comprise of insurance products offered by all the insurance partners of Policybazaar. The sorting is done in alphabetical order (Fund Data Source: Value Research). For a complete list of insurers in India refer to the Insurance Regulatory and Development Authority of India website, www.irdai.gov.in

Following are the details of the best pension plans by insurance companies:

Bajaj Allianz Life LongLife Goal

Canara HSBC Promise for Growth – Life Plan

Edelweiss Life Tokio Wealth Secure Plus

HDFC Life Click 2 Wealth

HDFC Life Smart Pension Plan

ICICI Prudential Life Signature Plan

ICICI Prudential Signature Pension Plan

Kotak e-Invest Retire Rich Plan

Max Life Flexi Wealth Advantage Plan

Max Life Online Savings Plan

Max Life SWP – Long Term Income Plan

PNB Goal Ensuring Multiplier Plan

Tata AIA Fortune Guarantee Pension Plan

Tata AIA Fortune Maxima

Bajaj Allianz Life LongLife Goal

Bajaj Allianz Life LongLife Goal

Key Features

The Bajaj Allianz Life LongLife Goal is a non-participating Unit-Linked Pension Plan (ULPP) with guaranteed life cover and annuity payout.

Benefits

Choose between LongLife Goal without Waiver of Premium and LongLife Goal with Waiver of Premium.

Benefit from the periodic return of Waiver of Premium charges and the option to reduce your premium.

Enjoy life insurance coverage until age 99 with Retired Life Income and Return Enhancer

Learn more about Pension Learn More

Canara HSBC Promise for Growth – Life Plan

Canara HSBC Promise for Growth – Life Plan

Key Features

Canara HSBC Promise for Growth is a retirement plan that helps you achieve your long-term financial goals while providing life insurance coverage for your family.

Benefits

Choose from three plans - Promise4Wealth, Promise4Care, or Promise4Life - based on your life stage needs.

Mortality Charges deducted during the policy term are added back to the Fund Value at maturity.

Receive Loyalty Additions every 5 years starting from the 5th policy year, and Wealth Boosters every 5 years starting from the 10th policy year.

Ensure continued policy coverage for your child in the event of your unfortunate demise.

Choose from a selection of 7 funds and enjoy unlimited switches if you opt for the Self-Managed Strategy.

Start your savings journey with premiums as low as Rs. 1,000 per month.

Learn more about Pension Learn More

HDFC Life Click 2 Wealth

HDFC Life Click 2 Wealth

Key Features

The HDFC Life Click 2 Wealth is a participating Unit-Linked Pension Plan (ULPP) with guaranteed life cover and loyalty additions.

Benefits

Receive a special addition of 1% of annualized premium for the first 5 years.

Get Mortality Charges back on maturity.

Choose from 13 fund options with unlimited free switching if you opt for the Premium Waiver.

Learn more about Pension Learn More

HDFC Life Smart Pension Plan

HDFC Life Smart Pension Plan

Key Features

HDFC Life Smart Pension Plan is a Unit Linked Pension Plan (ULPP) that helps you build a retirement corpus. It ensures regular income post-retirement and financial security during your golden years.

Benefits

Offers coverage up to 105% of all premiums paid, including top-ups.

Allows altering the vesting date and premium payment term as per your needs.

Rewards you with additional units to enhance your retirement savings over time.

Learn more about Pension Learn More

ICICI Prudential Life Signature Plan

ICICI Prudential Life Signature Plan

Key Features

A participating Unit-Linked Insurnace Plan (ULIP) with guaranteed life cover and loyalty additions.

Benefits

Enjoy benefits until 99 years of age with the Whole Life policy option.

Get back Mortality and Policy Administration Charges at maturity.

Choose from 4 portfolio strategies and a variety of funds across equity, balanced, and debt to suit your savings needs.

Learn more about Pension Learn More

ICICI Prudential Signature Pension Plan

ICICI Prudential Signature Pension Plan

Key Features

The ICICI Pru Signatrue Pension Plan is a Unit-Linked Pension Plan (ULPP) that helps you plan for a financially secure retirement. It combines market returns with flexibility to suit your retirement needs.

Benefits

Enjoy low charges, with premiums, policy fees, and mortality charges returned at vesting.

Add top-ups to increase your savings for future needs.

Access funds during emergencies like major life events or illnesses.

Delay your pension start date up to 80 years to grow your savings further.

Learn more about Pension Learn More

Kotak e-Invest Retire Rich Plan

Kotak e-Invest Retire Rich Plan

Key Features

The Kotak e-Invest Retire Rich Plan is a type of investment plan that combines investing your money in the market with some life insurance protection.

Benefits

Enjoy 100% allocation of your premiums.

Gain additional fund value from 25% to 200% of Life Cover charges deducted.

Opt for the Rising Star option for Triple Protection Benefit on the parent's death.

Ensure post-retirement expenses are covered with Retirement Income and Income Booster.

Learn more about Pension Learn More

Max Life Flexi Wealth Advantage Plan

Axis Max Life Flexi Wealth Advantage Plan

Key Features

A Unit Linked Insurance Plan (ULIP) designed to help you build a wealth portfolio for you and your loved ones for regular income during retirement.

Benefits

Guaranteed loyalty additions to your fund from the 8th year.

Choose between Wealth and Whole Life plans, various premium and policy terms, 5 investment strategies, and 12 funds.

Change your investment style anytime with unlimited free switches and premium redirections.

Learn more about Pension Learn More

Axis Max Life Online Savings Plan

Axis Max Life Online Savings Plan

Key Features

Axis Max Life Online Savings Plan is a unit-linked, non-participating traditional investment plan that provides both life cover and wealth creation benefits.

Benefits

Death benefit of the highest of Sum Assured, 105% of premiums paid, or Fund Value on death under Variant 1.

Under Variant 2 Immediate lump sum, Family Income Benefit, total Fund Value at term end, and company-funded premiums after death. Higher death benefits, lower returns.

Unlimited free fund switches, no Premium Allocation or Policy Administration charges. Only Mortality and Fund Management charges apply.

Learn more about Pension Learn More

Axis Max Life SWP – Long Term Income Plan

Axis Max Life SWP – Long Term Income Plan

Key Features

Axis Max Life SWP, which stands for Smart Wealth Plan is a whole-life insurance based retirement plan in India that is designed to provide income for a long period.

Benefits

Choose from Early Income, Early Income with Guaranteed Money Back, or Deferred Income Plans, all offering guarantees and cash bonuses.

Accrue and withdraw survival benefits as needed, with flexible withdrawal options.

Select an income period, including Whole Life Income, up to ages 100, 85, 75, 70, 65, or 60.

Learn more about Pension Learn More

PNB Goal Ensuring Multiplier Plan

PNB Goal Ensuring Multiplier Plan

Key Features

PNB Goal Ensuring Multiplier (GEM) is a Unit Linked Insurance Plan (ULIP) that combines life insurance coverage with investment options, aiming to help you achieve your long-term financial goals.

Benefits

Get back Fund Management, Premium Allocation, and Mortality Charges.

Exclusive feature for child-related benefits.

Adaptable premium payment options.

Premiums waived on death or critical illness.

Learn more about Pension Learn More

Tata AIA Fortune Guarantee Pension Plan

Tata AIA Fortune Guarantee Pension Plan

Key Features

Tata Fortune Guarantee Retirement Plan is an individual, non-linked, non-participating pension plan designed to provide you with a guaranteed income after retirement, along with life insurance coverage.

Benefits

Choose from 3 flexible plans: My Pension, Partner Pension, and Partner Pension Plus.

Enjoy a boost to your retirement corpus with guaranteed additions of 6% of the sum assured on vesting.

Special discounts for women, transgenders, and customers under 35 years of age.

Get life insurance coverage up to age 100 for your family's security.

Choose from multiple funds or the Enhanced SMART strategy for your investments.

Add optional riders to your ULIP policy for greater protection.

Learn more about Pension Learn More

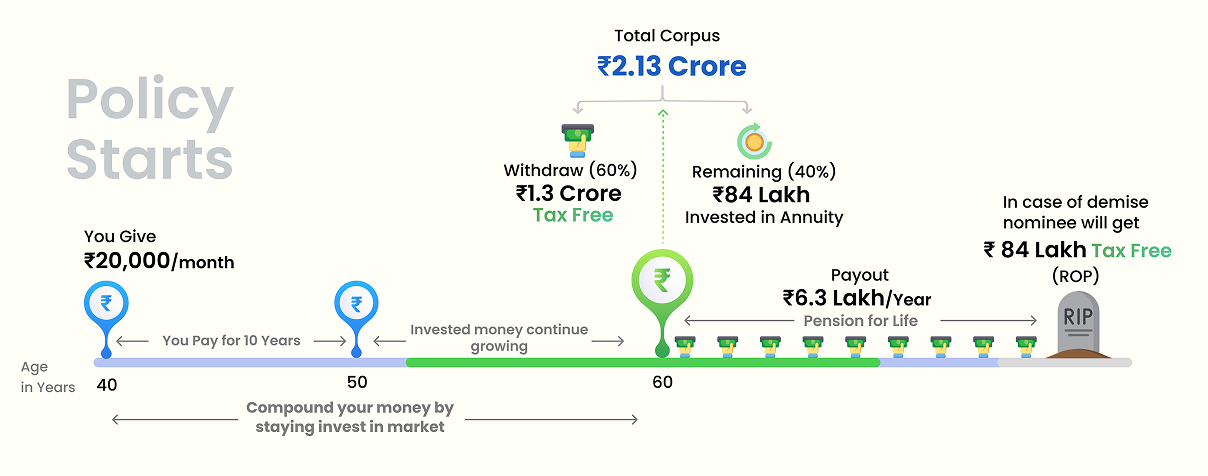

How Does a Pension Plan Work?

Let us explain the above infographic step-by-step:

Raghu is a 40-year-old working professional. He plans to buy a Pension plan to live a financially secure post-retirement life. The following steps will help her achieve a decent corpus at the retirement age:

Raghu's age at the time of policy purchase: 40 years

Investment for the next 10 years: Rs. 20,000 per month

Total invested amount: Rs. 20,000 X 12 X 10 = Rs. 24,00,000

This amount cannot be withdrawn for the next 10 years (till the time Raghu turns 60 years)

Total corpus accumulated at the age of 60: Rs. 2.13 Crores (with the help of the power of compounding)

Now, the corpus withdrawal system:

60% of Rs. 2.13 crores: Rs. 1.3 crores can be withdrawn Tax-Free (under Section 10(10A) along with clause 23AAB, at the age of 60)

40% of Rs. 2.13 crores: Rs. 84 lakhs must be invested in the Annuity

Annuity Payout system:

Raghu will get: Rs. 6.3 lakh every year (taxable under Section 17(1) and Section 56)

Nominee will get in case of Raghu's demise: Complete 84 Lakhs Tax-Free

Why Do I Need to Plan for My Retirement?

It is important to plan your retirement for the following reasons:

Uncertainty of Jobs:

Early retirement and market competition are leading to job losses.

You need to have enough savings if you wish to stop working before 60.

Healthcare Costs are Rising:

Medical care is rising every passing year.

Post retirement, you need a good corpus for your everyday health needs.

Increased Life Expectancy:

Life expectancy in India is now 70 years plus.

You need enough savings to last your whole retired life.

Cost of Living Hike:

Inflation hits hard, and you need to be prepared.

Your savings need to grow so you can afford things in the future.

Rise In Nuclear Families:

More people live in nuclear families and can’t rely on children for support.

You need to plan for your own retirement needs.

Types of Pension Plans in India

A wide range of pension plans in India are available to meet various financial needs. These plans have multiple classifications based on the plan structure and benefits.

Let's explore these pension plans in detail:

Pension Plans

Description

Deferred Annuity

Allows you to accumulate a corpus through regular or single premium payments Pension is provided after completion of the policy tenure

Offers tax exemption

1/3rd of the corpus is tax-free on withdrawal, while 2/3rd is taxable

Amount invested in Deferred Pension Plan is locked and cannot be withdrawn for emergencies

Suitable for investors with regular or lump-sum payments.

Immediate Annuity

Provides instant pension upon payment of a lump-sum amount

Policy nominee receives the money in case of the insured person's demise during the policy's tenure.

Life Annuity

Provides pension payments to the annuitant until their death

If the option of 'with the spouse' is chosen under the life annuity plan, the pension amount is transferred to the policyholder's spouse in the event of the policyholder's death.

Guaranteed Period Annuity

Offers annuity payments to the policyholder for specified periods, such as 5 years, 10 years, 15 years, or 20 years, regardless of whether the insured survives that duration.

Annuity Certain

Annuitant receives annuity payments for a specific number of years

Annuitant chooses the period of payment

If the annuitant passes away before receiving all complete payments, the annuity is paid to the policy's beneficiary.

Public Provident Fund (PPF)

Offers fixed, government-backed returns.

Features a 15-year lock-in period.

Provides complete tax exemption on returns (EEE).

PPF is designed for long-term financial goals, especially retirement.

Requires long term commitment of investment.

Suitable for investors seeking secure, tax-free, long-term savings.

Employee Provident Fund (EPF)

EPF offers fixed returns on employee and employer contributions.

EPS provides a fixed pension after retirement.

EPS pension may be limited and insufficient for all post-retirement expenses.

Suitable for individuals seeking a stable, post-retirement income.

Mutual Fund Schemes

Invests in a mix of equities and debt instruments.

Features a 5-year lock-in period.

Offers market-linked returns (no guarantees).

Equity component aims for higher long-term returns.

Debt component provides portfolio stability.

Subject to market volatility.

Suitable for investors seeking potential high returns with a diversified portfolio for retirement.

Pension Funds

Long-term pension scheme regulated by the Government under the Pension Fund Regulatory and Development Authority (PFRDA).

Offers better returns upon maturity compared to other plans.

Remains active for a specified period.

Policyholders can withdraw their annuity sum during the aggregation stage, providing financial security in emergencies.

Reduces reliance on banks for loans in such situations.

Whole Life ULIPs

Money stays invested for the entire life of the insured.

Partial withdrawals allowed upon retirement, providing tax-free income in whole life ULIPs.

Additional withdrawals can be made as needed.

Defined Benefit

Guarantees a specific retirement income for life

Calculations under Defined Benefit Plans are based on earnings and years of service with the employer

Defined Contribution

Retirement income not guaranteed, but contributions are

Both you and your employer can contribute

Your contributions determine your retirement savings

Retirement amount depends on contributions and investment returns.

See More Plans

Eligibility Criteria to Buy Pension Plan for Retirement

The three main eligibility criteria for purchasing retirement plans in India are really important because they help ensure you're on track for long-term financial security:

Entry Age:

In major cases, the minimum entry age for a Pension Plan is 18 years, but some plans require an entry age of 30 years. The maximum entry age is usually around 75 years.

Premium:

Premiums, in general, are the regular amounts paid throughout the policy period by the policyholder. Maturity returns at the end of the tenure depend on the regular premiums paid.

Vesting Age:

The age at which a policyholder begins receiving their pension is known as the vesting age, which is usually set at 40 years but can vary depending on the insurance provider.

Understanding the key benefits of a retirement or pension plan is essential, as these advantages help ensure financial stability, regular income, and a stress-free life after retirement:

Sum Assured:

The sum assured is a fixed amount guaranteed by the insurance company either at the time of maturity or to the nominee upon the untimely demise of the policyholder during the policy tenure. The amount is pre-decided at the time of the policy purchase and cannot be changed.

Tax Benefits:

Premiums paid qualify for tax deductions under Section 80C, and maturity proceeds can avail of tax exemption under Section 10(10D) of the Income Tax Act, 1961.

Annuity:

An annuity is like a plan where you pay once or over time, and in return, you get a steady income for a few years or even for the rest of your life.

Immediate Annuity: You start receiving income right after investing.

Deferred Annuity: Income starts after a certain period, usually after retirement.

Surrender Value:

The surrender value of a pension plan is the amount the insurance company will pay you if you terminate the pension policy before maturity. This amount receivable is low compared to the maturity amount, and hence, it is advisable not to surrender the policy.

Flexibility:

Pension plans provide various options for premium payment (lump sum or periodic) and annuity payouts (monthly, quarterly, or annually).

Risk Coverage:

Retirement plans may or may not include life insurance coverage based on the choice of the customer. In case the customer opts in for risk cover, it provides financial security to dependents.

Secure your Retirement today!

START INVESTING

₹6,000/month

GET PENSION

₹60,000/month+

INCLUDING LIFE COVER

+ Standard T & C Apply*

Pension Plan Buying Guide

Who Should Invest in a Retirement Plan Today?

Below is the list of people who should consider investing:

Individuals Seeking Tax Benefits:

Maximize tax savings under Section 80C and Section 10(10D).

Example: A salaried individual invests in a pension plan and claims a deduction of up to ₹1.5 lakh under Section 80C every year, effectively lowering their tax liability while securing a pension for the future.

Young Professionals:

Start early to benefit from compounding interest and build a secure retirement fund.

Example: A 25-year-old begins a pension plan with a modest monthly premium. Over 35-40 years, the accumulated corpus grows substantially, providing a comfortable monthly pension after retirement.

Self-Employed Individuals:

Take control of your retirement savings, as there are no employer-sponsored plans available.

Example: A freelance consultant invests in a pension plan, making flexible premium payments. Upon retirement, they receive a steady monthly pension, ensuring financial independence.

Employees Without Pension Benefits:

Don't rely solely on government schemes; secure your retirement with your own pension plan.

Example: An employee in a private company without a pension scheme starts a pension plan to build a retirement corpus, ensuring a monthly pension after retirement.

Those with Irregular Income:

Ensure financial stability in your non-earning years by building a reliable corpus.

Example:A small business owner with irregular cash flow invests in a pension plan, paying premiums when income is good, and still secures guaranteed pension benefits later.

People Aiming for FIRE (Financial Independence Retire Early):

Plan your early retirement; follow the trending FIRE Retirement path.

Example: A professional in their early 30s, aiming to retire by 45, channels a significant portion of their income into a pension plan. By the time they reach their FIRE target, they have built a sizable corpus that provides a steady pension, allowing them to cover living expenses and enjoy financial freedom decades before the standard retirement age.

Anyone Planning for Inflation-Protected Income:

Protect yourself against rising costs of living with plans offering increasing annuities.

Example: A retiree opts for a pension plan with a built-in inflation rider, ensuring their monthly pension increases by a fixed percentage every year to match rising living costs.

Factors to Consider Before Buying a Retirement Plan in 2025

Consider the following factors before buying a pension plan:

Retirement Age and Goals:

Determine your desired retirement age and lifestyle you want post-retirement.

Financial Needs:

Assess future expenses like healthcare, inflation, and daily living costs to estimate your required retirement corpus.

Plan Type:

Choose between traditional pension plans, market-linked plans (ULIPs), or annuity-based plans based on your risk appetite.

Premium Affordability:

Ensure the premium amount fits within your current budget.

Tax Benefits:

Evaluate tax deductions on premiums and exemptions on maturity.

Annuity Options:

Check for flexibility in annuity payouts—lump sum, monthly, or increasing annuities to combat inflation.

Life Cover:

Look for plans that provide life insurance coverage along with retirement benefits.

Flexibility and Add-Ons:

Opt for plans that offer withdrawal options, top-ups, or riders for critical illness or disability.

Plan Performance:

Analyze historical returns for market-linked plans and the financial strength of the insurer.

Loan Facility:

Check if the plan allows borrowing against the policy in case of emergencies.

Inflation Adjustments:

Ensure the plan offers features to keep up with rising costs, such as increasing annuities.

Current Debts and Loans:

Consider your current debts and loans and plan to minimize or eliminate them before retirement to avoid financial burdens in your post-retirement years.

What is the Right Amount to Save for Retirement?

Deciding the amount needed for retirement is a personal matter and depends on various factors. To estimate the amount, keep in mind the following factors:

Start Early

The earlier you start saving, the more time your money has to grow through compounding. Even small amounts invested consistently over a long period can accumulate into a significant retirement corpus.

Set a Savings Goal

Aim to save a specific percentage of your total earnings regularly:

Recommended target: Around 15% of your annual income (including any employer contributions) is a common benchmark.

Increase over time: As your income grows, try to increase the proportion you save to build a larger corpus.

Target Your Desired Lifestyle

Your retirement corpus should support the lifestyle you want post-retirement. Consider:

Do you want to travel frequently?

Will you maintain your current living standards?

Are there any expensive hobbies or activities planned?

A more luxurious lifestyle will require a higher savings target.

Account for Inflation

Inflation reduces the purchasing power of money over time. When estimating your retirement corpus:

Assume an average inflation rate (e.g., 6-7% annually).

Ensure your savings and pension income grow at or above inflation to maintain your lifestyle.

Diversify Your Investments

Spreading your retirement savings across different asset classes reduces risk and improves returns:

Include insurance pension plans, equities, fixed income, and other instruments.

Diversification helps balance growth potential and safety.

Save Consistently

Consistency in savings is key:

Make regular contributions (monthly, quarterly).

Avoid skipping payments even during financial challenges to maintain momentum.

Use a Retirement Calculator

Leverage online pension plan calculators to:

Estimate how much you need to save based on your age, income, and retirement goals.

Adjust variables like inflation rate, expected returns, and retirement age for personalized planning.

Review and Adjust Regularly

Your financial situation and goals may change:

Review your retirement plan annually or after major life events.

Adjust your savings rate, investment mix, or retirement age accordingly.

What is Retirement Planning?

Retirement planning is the process of preparing your finances for the retirement stage of your life. It involves setting goals, estimating your income needs, and taking steps to accumulate and manage funds to support those needs throughout your retirement years.

It is important to have a well-thought-out retirement plan that considers factors such as inflation, healthcare costs, and changing lifestyle needs. Start planning for retirement as early as possible to accumulate enough funds for future expenses and maintain a standard of living during retirement years.

Pension Calculator

Pension Calculator

How much do you need to save for retirement?

₹

₹ 20,000

₹ 25,000

₹ 30,000

Calculate

Monthly Expenses in 2025₹ EditDone

Inflation Rate

Today 2025 Your expenses today in 2023, at the age of 34 Yrs

Your expenses in 2043, at the age of 55 Yrs

For a monthly pension of ₹77,300 you need to invest

₹14,300/month

Calculated as per past performance of 15%

View PlanRecalculate?

Importance of Retirement Planning for Different Ages

The importance of planning changes with different stages of life. Knowing these stages can help you make smart financial decisions for a comfortable retirement.

Let us have a look at the significance of retirement planning based on age and life stages:

“Start young, retire strong.”

Start early to build a strong financial foundation.

Invest 10-15% of your income in a pension plan.

Use compound interest to grow your savings.

Invest aggressively in growth-oriented assets.

Increase contributions as your salary grows.

View Plans

“Time to turn up the savings dial.”

Focus on balancing growth and stability in investments.

Save 15-20% of your earnings for retirement.

Fill any gaps in your savings from earlier years.

Increase contributions to retirement savings.

Focus on growing your investments for a secure future.

View Plans

“Finish strong and steady.”

Prioritize safeguarding your accumulated wealth.

Save 20-25% of your income in stable, high-yield investments.

Boost your retirement fund as you near retirement.

Shift towards low-risk investments for steady returns.

Make every contribution count.

View Plans

“Preserve and enjoy.”

Manage funds to ensure a stable income post-retirement.

Shift to low-risk, income-generating investments.

Protect your savings while enjoying retirement.

Minimize expenses to preserve savings.

Ensure your funds support a comfortable lifestyle.

View Plans

How to Buy a Retirement Plan Online in 2025?

To buy a retirement plan, you will want to start by finding out about your financial goals, then follow these steps:

Step 1-

You can check retirement plans on this page or through the Policybazaar homepage.

Step 2-

Check the features and premiums of different plans to find the best fit for you.

Step 3-

Pick and choose the most suitable plan that aligns with your goals and needs.

Step 4-

Think about adding on features or adjusting coverage if needed to modify the plan according to your situation.

Step 5-

Make your payment online and receive confirmation about your retirement plan.

Various Payment Modes Allowed (Regular/ Limited/ Single)

Fixed Yearly Deposit Required

Flexible Contributions Allowed as per NPS Tier Rules

Lump Sum Premium Only

Partial Withdrawal Amount

Allowed after 7 years

Allowed after 3 years

Lock-in Period

Varies as per plan

15 years

60 Years of Age

40 Years of Age

Returns

Returns

9 - 15% p.a.

7.1% p.a.

9 - 12% p.a.

Guaranteed Annuity

Risk Factor

Moderate

Low

Moderate

Low

View Plans

Conclusion

Pension Plans play an important role in securing financial stability during retirement. With a diverse range of options, individuals can choose pension plans according to their choices to meet specific needs, ensuring a comfortable and worry-free post-retirement life. Planning ahead and selecting the right pension plan are essential steps towards a secure and fulfilling retirement journey.

Frequently Asked Questions

Can I start my pension at 55 and still continue working?

Yes, you can begin receiving your pension at any age—even if you're still employed. Pension or retirement plans let you decide when to start the payouts, regardless of your actual retirement.

Is it possible to have more than one pension plan?

Yes, you can invest in multiple pension plans. However, be mindful that there’s a cap on the total contribution if you want to claim tax benefits across all the plans.

Do pension plans in India stop providing benefits after the policyholder dies?

Not necessarily. Most annuity plans include a life cover. In the event of the policyholder's death, the nominee typically receives the policy benefits and may either withdraw the full amount or use a portion to buy an immediate annuity.

If I have a provident fund, do I still need a pension plan?

It’s wise to diversify your retirement savings. While a provident fund helps you save, it restricts how much you can withdraw upon maturity. A large part must go towards an annuity.

In contrast, pension plans help you build a retirement corpus with more flexibility—you can access the full maturity amount without strict withdrawal limits.

Which should be a priority—saving for retirement or my child’s education?

It’s wise to begin saving for retirement as soon as you start earning. Early planning helps reduce financial pressure in the later stages of your career. At the same time, you can start building an education fund for your child from the time they’re born. Both goals can be pursued simultaneously with a balanced investment approach.

What is LIC’s new pension plan (LIC Smart Pension Plan)?

This is a single-premium, non-par, non-linked pension scheme.

It offers flexible annuity options for both single and joint life annuities.

The plan is designed to provide retirees with a steady and reliable income stream.

It has various annuity payment options, such as monthly, quarterly, half yearly or yearly.

It also has options for people that are NPS subscribers.

Customizable with advanced annuity, liquidity, and accumulation options.

What is the Universal Pension Scheme?

The Universal Pension Scheme (UPS) is a proposed initiative by the Indian government aimed at providing social security to a wider range of citizens, particularly those in the unorganized sector. Here are its key aspects:

Goal:

To create a more inclusive and comprehensive pension system that extends coverage to individuals who currently lack access to traditional pension schemes.

Objective:

To provide financial security during old age by ensuring a regular income stream for a larger segment of the population.

What is the Unified Pension Scheme (UPS)?

The Unified Pension Scheme is a new pension scheme introduced by the Indian government for its government employees. It aims to provide a more secure post-retirement financial situation by offering assured pension benefits.

Which is the best pension scheme?~

The best scheme depends on your goals. Popular options include Unit-Linked Pension Plans (ULPPs), National Pension System (NPS) for flexibility and returns, and Annuity Plans for guaranteed income.

What are pension plans in India?

Pension plans are financial products that provide regular income after retirement along with a life cover to ensure financial stability. They help you to accumulate savings during your working years, which can be converted into a pension upon retirement.

What is Linked and Non-Linked Pension plans?

Linked pension plans invest in market-linked instruments, offering potentially higher returns but with more risk. In contrast, non-linked pension plans provide guaranteed returns and are less risky, often providing fixed interest rates.

Who can invest in retirement plans in India?

Anyone can invest in retirement plans in India, including salaried individuals, self-employed persons, and even Non-Resident Indians (NRIs). However, specific schemes may have eligibility criteria.

Can I withdraw money from my retirement plan before retirement?

Generally, early withdrawals from retirement plans are restricted. However, some plans like HFDC Life Pension Plans allow partial withdrawals during accumulation phase under specific conditions after a certain period.

What happens to my pension plan if I change jobs?

If you change jobs, your pension plans like ULPPs remain intact. For pension schemes like EPF, you can either transfer your EPF balance to your new employer and for NPS scheme, you can continue your NPS account without disruption.

Are pension plans in India inflation-adjusted?

Most traditional pension plans do not automatically adjust for inflation. However, market-linked options like Unit-Linked Pension Plans (ULPPs) and NPS can potentially provide returns that outpace inflation due to their investment in equities and debt.

Can I nominate someone in case of my demise?

Yes, you can nominate a beneficiary for your pension plan. In the event of your death, the nominee will receive the accumulated benefits or death benefits as stipulated by the plan.

Are retirement plans in India regulated?

Yes, retirement plans in India are regulated by the Insurance Regulatory and Development Authority of India (IRDAI) and the Pension Fund Regulatory and Development Authority (PFRDA), ensuring investor protection and compliance with standards.

What do you mean by Participating and Non-Participating Pension plans?

Participating pension plans allow policyholders to share in the insurer's profits through bonuses. In contrast, non-participating plans do not offer bonuses but provide guaranteed returns based on fixed premiums paid.

How do I get a ₹50000 monthly pension?

For a monthly pension of ₹50,000, you need to invest about ₹1,700 per month for 30 years at a 15% annual return. This will grow to around ₹1.26 crore at the age of 60 years, enabling you to secure the target pension through an annuity.

Is pension plan better than FD?

Pension plans provide long-term income, tax benefits, and life cover, while FDs are better for short-term savings with fixed returns.

Is pension taxable?

The taxability of your pension corpus depends on the type of pension plan. For ULPPs, you get tax-free maturity amount under Section 10(10D) if your annual premiums are below ₹2.5 lakhs. However, the payouts from annuity plans are taxable as per your income tax slab.

How to avoid TDS on pension?

To avoid Tax Deducted at Source (TDS) on pensions, ensure that your total taxable income remains below the taxable threshold or submit Form 15G/15H to your bank if applicable.

How to choose a pension plan?

When choosing a pension plan, consider factors like your age, financial goals, risk appetite, expected retirement age, and whether you prefer guaranteed returns or market-linked growth. Comparing different options can also help make an informed decision.

How to get ₹2 lakh per month pension?

To achieve a monthly pension of ₹2 lakh, invest approximately ₹7,000 per month at the age of 30 years at a 15% annual return. This will accumulate around ₹4.91 crore at the age of 60 years, allowing you to receive the desired pension of ₹2 lakh after purchasing an annuity.

˜Top 5 plans based on annualized premium, for bookings made in the first 6 months of FY 24-25. Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. This list of plans listed here comprise of insurance products offered by all the insurance partners of Policybazaar. For a complete list of insurers in India refer to the Insurance Regulatory and Development Authority of India website, www.irdai.gov.in *All savings are provided by the insurer as per the IRDAI approved

insurance plan.

# The investment risk in the portfolio is borne by the policyholder. Life insurance is available in this product. The maturity amount of Rs 1 Cr. is for a 30 year old healthy individual investing Rs 10,000/- per month for 30 years, with assumed rates of returns @ 8% p.a. that is not guaranteed and is not the upper or lower limits as the value of your policy depends on a number of factors including future investment performance. In Unit Linked Insurance Plans, the investment risk in the investment portfolio is borne by the policyholder and the returns are not guaranteed. Maturity Value: ₹1,05,02,174 @ CARG 8%; ₹50,45,591 @ CAGR 4%

^The tax benefits under Section 80C allow a deduction of up to ₹1.5 lakhs from the taxable income per year and 10(10D) tax benefits are for investments made up to ₹2.5 Lakhs/ year for policies bought after 1 Feb 2021. Tax benefits and savings are subject to changes in tax laws.

¶Long-term capital gains (LTCG) tax (12.5%) is exempted on annual premiums up to 2.5 lacs.

++Source - Google Review Rating available on:- http://bit.ly/3J20bXZ

**Returns are based on past 10 years’ fund performance data (Fund Data Source: Value Research).